The end of the beginning: Steth

Article #1 of my thoughts on financial scenarios

It’s priced in. It’s always supposed to be. What if it wasn’t, though? Is that an opportunity, or is it betting behind smoke and mirrors?

Getting paid to hold Ethereum - who would be upset? The rationalists who know the casino doesn’t give free chips without a cost.

We’ve all played on the online casinos that offer a bonus for the first deposit. Get a $25 reward for a $50 deposit - what a deal! The deposit goes through, and the casino says the $25 bonus can only be used on rigged slot games with a 30x rollover. In other words, the $25 is not going to be withdrawn.

What is Lido?

To understand why Steth is so appealing to people, an understanding of the Ethereum staking mechanism is required. When Ethereum is staked, the tokens are dedicated to validating the Beacon Chain by storing blocks and adding data. In return for this, interest is given on the Ethereum - currently around 4.4% annually but shifting around. Furthermore, when the Ethereum is staked, it is locked until an event that happens after The Merge (estimated 6-12 months after?).

Lido is a valuable product built for a niche consumer base. Stake ETH and get a claim on the ETH deposited + yield. The only catch is that 10% of the yield is taken and distributed to the Lido treasury. This system works for people with < 32 ETH or incapable of running a validator. It’s a tradeoff that works because it’s a symbiotic relationship. The users benefit from getting the yield they would otherwise not have access to, and the Lido treasury benefits from the fees.

So in that current state, the relationship makes sense, and there is no irrationality behind it. So why are there hundreds of addresses with thousands of ETH staked through Lido then, and Celsius with 450k+ itself? Surely addresses of that nature wouldn’t sacrifice millions of dollars of yield to not manage validators.

People staking through Lido are given a token called Steth that is fully backed 1:1 by ETH. This was supposed to solve the problem of the Ethereum being locked after staking. Get the benefits of staked ETH but still get a semi-liquid token. Steth held a 1:1 peg for a long time with ETH, but that peg only remains so long as the demand for Steth > sell pressure. This system works fine in a bull market because people are bullish on Ethereum and want to hold it. In a bear market, though, these people with Steth may wish to sell to USD, and there won’t be enough demand for it to keep the peg intact.

Lido attracted billions of TVL. Even at recessed prices of < $1000 per ETH, their total value locked still sits comfortably over $4B.

Liquidity

With Billions of TVL comes the need for ample liquidity. How else can the price of an asset be expected to be trading at similar levels to another asset without a redemption method? The short answer is no; it cannot happen.

Lido has a fun way of incentivizing liquidity - they use emissions on their “governance” token to reward holders who provided liquidity. Quotes around governance because governance tokens are a well-designed meme and don’t work efficiently. When this address owns 7% of the supply - most votes do not matter. Incentivizing liquidity with other tokens work well until it doesn’t.

$LDO, the governance token for Lido, is down significantly against Ethereum this year. There are many reasons for this, but the most important is that these people providing mercenary liquidity to the Steth-ETH pool are not friends. They are there to farm the token, sell it, and move on. So, naturally, as LDO endures this sell pressure, the token goes down in value, and the expected yield for the liquidity providers decreases. This results in two things.

First off, these liquidity providers pull their liquidity. This means that not only is Lido back to stage one (they need liquidity for the token to be liquid but don’t have it), but they have also sacrificed the price of their governance token. Additionally, the loyal supporters who are there to help the protocol and care about voting feel betrayed because they have watched their investment go down 90%+ at the benefit of mercenary liquidity providers.

Second, when these liquidity providers pull out their liquidity, they need to offload those tokens. As governance emissions produce less yield, people want out. Sometimes, these liquidity providers cannot sell their tokens because everyone is trying to sell into a rapidly decreasing liquidity pool. This is similar, if not the same, to a bank run.

I don’t believe Lido liquidity will ever fully suffer a bank run because each Steth is fully backed. The discount relative to ETH should be +EV for buyers at some point. What discount is that, though? 5%, 15%, 25%?

The first issue remains, though. Steth is supposed to be a liquid staking alternative. Is it, though? Curve only has 114k ETH in the liquidity pool. That isn’t even anywhere near the total amount of Steth in existence. So how liquid is it really if there are more tokens than liquidity?

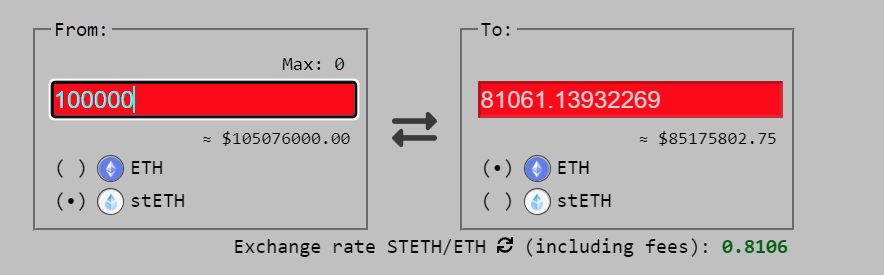

The curve pool has seen major withdrawals of ETH over the last many months. As liquidity dries up, the pool imbalance grows. Currently, the pool is in an 82-18 imbalance. 82% of the pool comprises Steth and 18% of ETH. Despite the pool imbalance, Steth is still trading at .9366 of an Ethereum token. How is there only a 6.5% discount when the pool is severely imbalanced? Well, Curve liquidity is known to be tight. A 100k Steth sell would only drop the ratio to .8106. Eventually, though, this liquidity is going to dry up.

$LDO incentives are the smoke and mirrors preventing liquidity from ultimately going away and subsequently a fair market price for Steth.

Leverage and Liquidations

Because people in crypto are obsessed with leverage, they turned Steth into a product that could be leveraged to earn even more yield on Ethereum. Since Steth was priced 1:1 with Ethereum for a long time, people set up high leverage positions with liquidations at .8 ETH/Steth or even higher in some cases. This was done by depositing Steth into platforms like Aave and borrowing ETH against those positions. Then, swap ETH to Steth, deposit that and borrow again. The more the process is repeated, the higher the leverage is and the higher the ratio is at which the position gets liquidated. Lido sums it up very well here.

The issue with this is that eventually, these positions will get liquidated when the ratio drops to a more rational level. With the liquidity already dropping rapidly, can the market handle liquidations in the size of hundreds of millions?

I do not think the market will be able to handle liquidations of this size in this macro-environment. A liquidation cascade will happen if even one of these prominent positions gets liquidated. With limited buy demand for Ethereum in this current market coupled with low confidence, some very cheap Steth could be seen soon. This is something to keep an eye out for, which leads me to the next section.

How can Steth be shorted?

Unlike many cryptocurrencies, there are no perpetual futures for Steth. This makes shorting a complicated feat that can only be achieved through the following system:

Lock up collateral in a platform

Borrow Steth

Convert the Steth to ETH

Buy back the Steth when the ratio drops and profit from the extra ETH

However, the primary money market for Steth is Aave, which does not support Steth borrowing. Euler Finance is an alternative to Aave, which has enabled Steth borrowing. However, because of the rise in popularity of this short opportunity, it is expensive to borrow Steth. At current rates, borrowers need to pay 5.37% interest annually + the 4% interest at which Steth grows (because when Steth is swapped into ETH, the Steth yield is forfeited). Furthermore, with Steth already trading 6.5% under ETH, it is risky to short here because the position is down an upfront 6.5% on the initial trade and 9.37% annually, waiting for the Steth: ETH ratio to further widen.

When do I want to buy Steth?

Unlike other individuals, I do not think Steth can be compared to products like GBTC or ETHE. Both GBTC and ETHE are trading at 35%+ discounts relative to their base asset. Even though these ETFs are fully backed 1:1 by their base assets, they trade at a discount because until the SEC approves the shift to a spot ETF or Barry Silbert (CEO of Greyscale) unwinds the fund, redemptions are not possible. This is *very* similar to Steth because both situations rely on an external feat to be achieved for redemptions to be allowed.

The difference between the two products comes in the fee structure. GBTC charges a 2% annual performance fee and ETHE 2.5%. This means that the trade is losing money by holding those two products in anticipation of an arbitrage opportunity. On the other hand, Steth pays the trade roughly 4% annually.

So, how can the golden ratio be accurately determined if Steth cannot be compared to GBTC/ETHE? To figure this out, I need to know the minimum discount the average investor is fine locking their funds indefinitely in anticipation of the arbitrage + discount. I don’t know what that number is yet: but I think once the liquidity dries up and some liquidations are seen, the market will price Steth correctly for the first time.

Who is at fault?

I don’t believe Lido is at fault for what is occurring here. From the start, Lido made sure it was widely known that Steth was *not* supposed to be pegged 1:1 to Ethereum. Locked staking alternatives should always trade at a discount to the unlocked version, and they clarified that. Unfortunately, the market priced it incorrectly because of the $LDO incentives coupled with the biggest crypto bull market in history. Demand for yield on Ethereum was so great that any discount in the pair was snapped up because people thought they were getting a deal.

I also do not think Steth broke its peg because of contagion from UST. Instead, I believe UST sped the process up because people realized that pegged tokens are not always worth the currency they are pegged to.

There is no one at fault here besides the market for pricing it wrong the first time.

Contagion

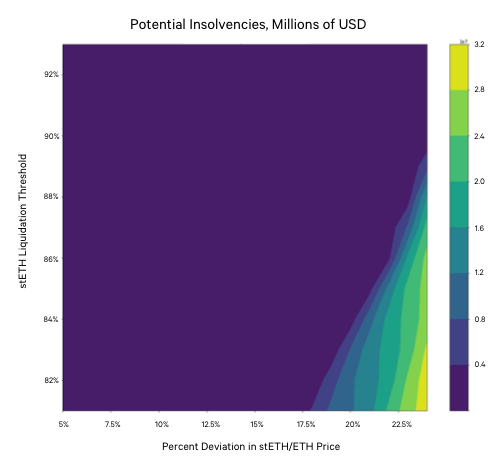

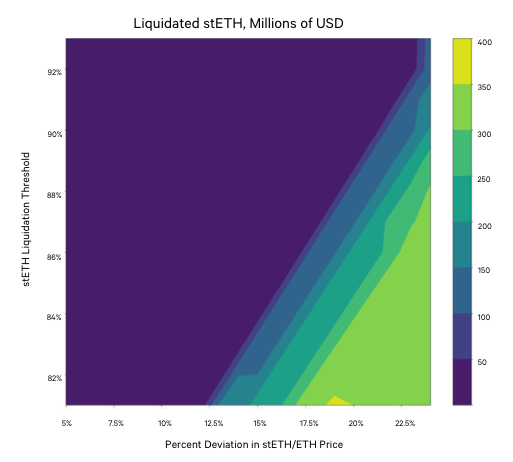

If doomsday comes, will DEFI be able to survive? Steth is a vast product rooted in many of the major dAPPS, and if liquidations spiral downwards, it could leave some protocols insolvent.

For example, Aave uses Steth as collateral in its lending market. With evaporating liquidity and high leverage, this creates a serious systematic risk for bad debt if the protocol cannot successfully liquidate the leveraged positions.

(The images above are used from an Aave proposal here)

Aave recognizes this: see ongoing conversations and proposals to solve this here. While Aave is known to be quick on its feet and push solutions to issues fast, not all protocols are like this. I fear that many lending dAPPS are too complacent with their collateral structures and thus are not prepared for a Steth liquidation cascade. Market Manipulation is also possible because of the tight leverage, and attempts at this have already happened by Alameda (a trading fund connected to FTX).

If DEFI wants to survive, the lending dAPPS that act as a crux to DEFI need to alter their collateral structures and take measures to ensure they can adequately liquidate positions if required. If they don’t, Defi could be wiped out as lending markets take on hundreds of millions of bad debt and kill the ecosystem.

What role can Steth play in the future?

Steth has a role in the Ethereum ecosystem, but not its current position. It should be considered as a token purchasable at a discount and gain interest, so long as the ETH is locked. In its current form, it is highly harmful to DEFI, and protocols should work to unwrap the prominent place Steth holds slowly.

Steth is *not* ETH, and they should not be treated as the same.

Final thoughts

Lido is an innovation that has brought a lot of success to Ethereum and allowed for many complex opportunities. While Steth is trading at a higher ratio than it should be, Lido is not responsible that the market is irrational. I hope to see them continue to innovate and propel themselves further. I am incredibly excited to see how redemptions will impact Steth when Ethereum unlocks finally occur.

W essay twin

piss man